Insurance provides an effective means of mitigating financial risk. By understanding the various types of policies available to you, it is possible to select coverage tailored specifically to meet your personal requirements and budget constraints.

This article will highlight five essential types of insurance coverage, namely auto, life, health, home/property/long-term disability and long-term disability policies. Each will be explored with details about what it covers and its operation.

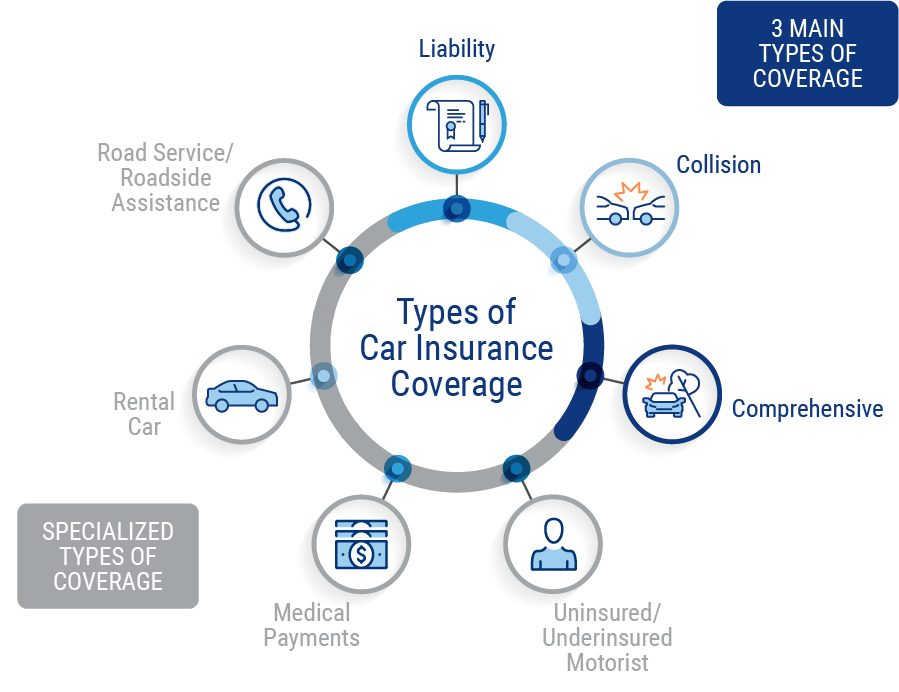

Automobile Insurance

Insurance is an agreement between an insurer and policyholder to cover specific forms of loss. Most people protect themselves financially in case of accidents or natural disasters with some form of coverage for cars, health, homes and lives – from liability coverage for bodily injury and property damage, comprehensive and collision coverage as well as medical payments coverage. Six major types of car policies exist that provide this essential protection: liability for bodily injury/property damage liability/comp comprehensive/collision (CC/cr), comprehensive/collision (CC/cr)/medical payments policies etc.

Liability coverage is mandatory in many states and serves to cover other people’s damages when you’re at fault in a car crash. There are two categories of limits associated with this insurance – bodily injury per person and property damage per accident. You may opt to purchase additional coverage beyond what the minimum state requirements offer, which can often be advantageous.

Collision insurance pays to repair your vehicle following an accident, regardless of who was at fault. Additionally, this policy protects it when an unplanned event such as tree branches falling on it or theft occur – or damage from severe weather such as hail and windstorm. Collision coverage may even be required when leasing or financing a car.

Medical payments (Med Pay) or personal injury protection (PIP) is designed to cover your and the passengers’ medical expenses following an accident, as well as lost wages from time lost due to being injured and no longer working. Medical payments coverage is required by some states while optional in others.

Uninsured/underinsured motorist (UM/UIM) coverage protects you and your passengers if they are hit by an uninsured or underinsured driver; some policies also include coverage against property damage caused by such drivers.

Homeowners insurance provides protection for both your home and belongings against damage or theft, while providing temporary housing if needed. Furthermore, it can compensate you if someone is injured on your property and sues for negligence – an advantage which you shouldn’t neglect when protecting the assets you care for so dearly.

Life Insurance

Life insurance is one of the most essential forms of coverage. A loved one’s death can create financial strain for survivors, so life insurance provides a cost-effective solution. But with various policies available and prices that range accordingly, finding one suitable to both your needs and budget may prove challenging. From providing end-of-life expenses coverage to covering debt or leaving an inheritance behind for loved ones there may be one suitable plan out there to suit all goals.

Life insurance generally falls into two main categories: term and permanent (also called whole). With term life policies lasting a specific length of time before paying out the death benefit upon death of an insured within that term; in contrast with this type of policy, permanent policies will continue paying out death benefits as long as premiums remain paid; term policies also offer flexible payment terms so beneficiaries receive payments when death occurs during that term.

Permanent life insurance policies often feature a cash value component, an investment portion that can be borrowed against or cashed out at any time. Although more costly than term life policies, they often provide greater coverage in return. Examples of permanent life policies include whole, universal, indexed universal and burial policies.

Some life insurance plans can even help you prepare for retirement. A final expense policy, for instance, provides protection for funeral costs and end-of-life expenses while leaving beneficiaries with an affordable sum upon your death. Though these policies often offer lower coverage limits than traditional forms of life insurance policies, they provide valuable peace of mind if only limited amounts of protection is necessary.

When searching for life insurance, it’s essential to compare rates and benefits in order to find the most economical policy. Furthermore, consider any life coverage provided through your employer that could prove more cost effective than purchasing an individual policy on your own.

Health Insurance

Health insurance provides essential financial protection for hospitalization, doctor visits, prescription medicines and other medical expenses. Coverage may come from either private insurers or from government-backed programs like Medicare, Medicaid and the Veterans Health Administration.

Employers frequently offer health insurance as part of their benefits package, with coverage depending on your priorities and budget. Key types include PPO plans, HMO plans and HDHPs (high deductible health plans).

Preferred provider organization plans (PPOs) provide you with access to healthcare providers within their network for reduced costs, although you may still be able to receive care outside this group – though at an increased price. PPOs require you to name a primary care physician who will monitor and coordinate all aspects of your healthcare, and refer you as needed to specialists.

Health maintenance organization (HMO) plans typically offer access to a broad network of healthcare providers and emphasize preventive medicine, helping HMOs manage your costs and lower out-of-pocket expenses. They typically impose a deductible before coinsurance starts covering expenses.

Exclusive provider organization plans (EPOs) typically feature smaller networks than PPOs but often provide lower deductibles and copayments. While they may cover out-of-network care at additional costs, primary care referral may be necessary in order to access specialists.

Catastrophic health insurance provides another great safety net in case of unexpected medical emergencies or chronic conditions, with low premium costs that cover only the most costly treatments – potentially helping avoid expensive financial bills in case something unexpected comes up.

As you assess your insurance needs, take some time to consider how your lifestyle and priorities fit with those that matter. That way, you can find policies tailored specifically for you that protect both family members and finances for the long haul. When it’s time to discuss which coverage might best meet your unique situation, reach out – we are more than happy to answer any queries or help get the conversation underway towards a secure future!

Homeowners Insurance

Homeowner’s insurance provides property and liability protection for your residence and belongings against damage or loss, with most policies also covering personal liability issues. Mortgage lenders usually require homeowners insurance as a prerequisite to qualifying for home loans, though policy specifications can differ by provider; all policies include an “indemnification page,” detailing dollar limits and deductibles in your coverage agreement.

Additions to a homeowners’ policy may include ordinance or law coverage, which covers the additional cost associated with rebuilding to meet updated local building codes or requirements that were not in place when your house was originally built, water damage and sewer backup protection, and identity theft protection.

Most homeowners assume their homeowners’ insurance will cover everything, but that isn’t necessarily true. There are certain natural disasters – like floods and earthquake damage – which aren’t covered under standard homeowners’ policies – you may need additional specialized policies for such events.

Your homeowner’s insurance may not cover the full value of your belongings either. Exclusions typically apply for jewelry and fine arts pieces; you may need a separate policy for these. In general, the replacement cost minus depreciation of most possessions are covered; however, they usually don’t cover fully-priced electronics appliances and other high-valued items such as furniture.

Other structures coverage may be included in your policy to protect unattached buildings on your property, such as fences, sheds and detached garages. Some policies also offer coverage for guest houses or rental properties you use for short-term rentals.

Liability coverage typically provides for medical expenses for any individuals injured on your property, and compensation for damage to their belongings. An umbrella liability policy could provide extra liability protection. Generally speaking, no discriminatory practices should occur between insurance providers when offering or renewing homeowners’ and auto policies or providing or renewing them; such discrimination cannot take into account factors like race, religion, gender, age, sexual orientation marital status disability public assistance receipt.

{kind=link}

{kind=link}