Health insurance is a legal contract which reimburses or covers payments related to health care expenses, either directly through an insurer or employer-sponsored plan, or indirectly via government programs like Medicare and Medicaid.

This analysis employs two methodologies to estimate the number of individuals who would face denials, significant mark-ups or carve-outs due to preexisting conditions. The first approach uses eligibility guidelines from state high-risk pools that existed prior to ACA implementation as a baseline estimate of this scenario.

Costs for Pre-Existing Conditions

Pre-existing conditions refer to illnesses, injuries and health conditions that existed prior to purchasing health or life insurance policies. Such pre-existing conditions can have a dramatic impact on costs due to having to pay more out-of-pocket for care related to them.

Under the Affordable Care Act (ACA or Obamacare), pre-existing conditions no longer pose a barrier to affordable coverage. Under its provisions, insurance companies cannot deny coverage due to pre-existing conditions; all marketplace plans must cover any associated costs without increasing premiums accordingly.

However, if the Affordable Care Act (ACA) is repealed and replaced with legislation such as the Better Care Reconciliation Act (BCRA), many of these protections could be lost – leading to higher premiums than ever for people with pre-existing conditions and even denial of coverage altogether.

If a person with a pre-existing condition cannot secure health insurance, they will not have access to necessary care and treatments that could have a dramatic impact on their overall well-being and could exacerbate other medical conditions over time. This situation can be especially challenging for families as the cost of treatment can strain budgets and lead to debt; leading to greater hardship and strain for all concerned.

Many Americans live with pre-existing conditions, and the prevalence is growing more prevalent as we get older. Heart disease, cancer, asthma, depression and chronic obstructive pulmonary disorder (COPD) are some of the more frequent ones; having these and other conditions can be costly; having coverage might even prove difficult for some individuals with these preexisting issues.

Under current law, pre-existing conditions do not stand in the way of most individuals being able to secure affordable health insurance; most can enroll through their employer plan or directly in the marketplace with an individual policy. In previous decades, individuals with pre-existing conditions often relied on State high-risk pools because private insurers would not cover them.

Experience rating is an issue for small businesses as their rates can rise whenever one employee becomes sick or injured, forcing them to adjust coverage if one of their workers develops chronic health conditions that necessitate reduced coverage or discontinuing coverage altogether.

Pre-Existing Condition Exclusions

Pre-ACA, individuals with preexisting conditions seeking health insurance through the individual market typically faced significant obstacles. If they could locate an insurer, they might face expensive premiums (which could be “rated up”) or exclusion periods that prevented coverage for their health conditions for an indeterminate amount of time – usually six months or longer of prior coverage, time since cancellation of coverage and other factors were all key components to consider when considering eligibility for coverage for preexisting conditions.

The Affordable Care Act places strict limits on when insurance companies can exclude pre-existing conditions from new policies. Specifically, insurers cannot exclude conditions diagnosed, treated or prescribed within three to six months before an effective date, or during which applicants were actively seeking medical care for covered illnesses. Furthermore, pre-existing condition exclusions cannot be used on existing policies either.

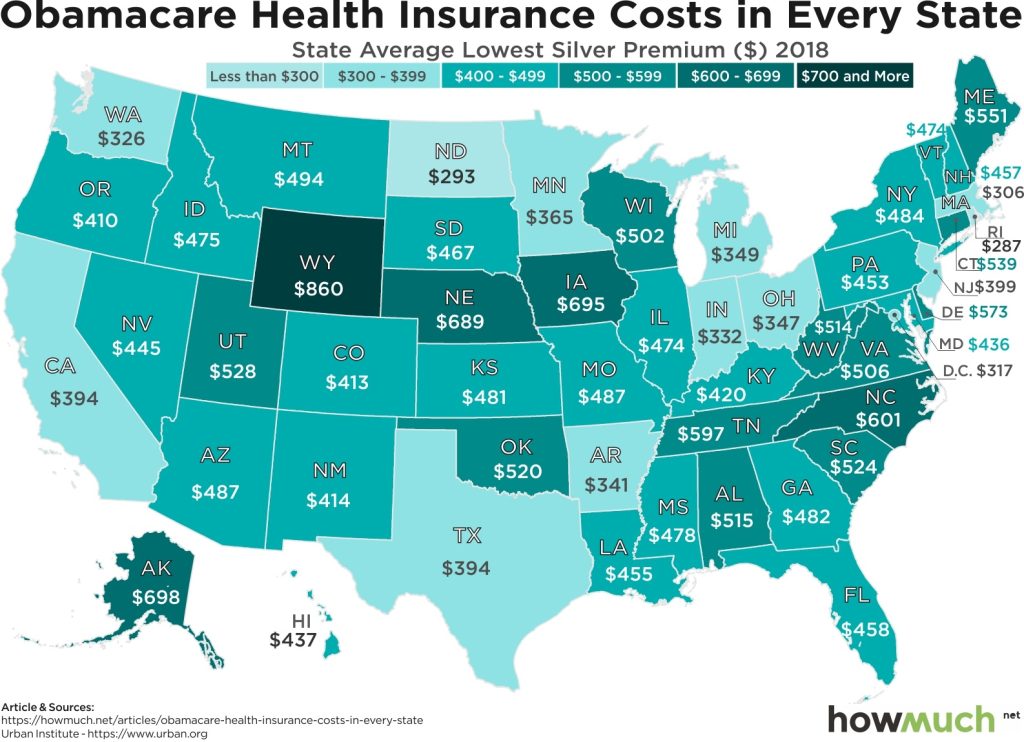

Individually, this change has made an immense difference for many individuals. As shown by the chart below, pre-ACA, one third to one fifth of individuals purchasing their own health insurance had conditions which would have caused their coverage application to be denied under previous insurers’ criteria for individual and high-risk pools – this figure has significantly decreased thanks to reforms brought about by the Affordable Care Act (ACA).

Still, many Americans continue to face significant difficulties in securing affordable coverage. A Kaiser Family Foundation analysis based on medical Expenditure Panel Survey data indicates that at least 22% of non-elderly adults may have conditions declinable under previous underwriting rules in individual insurance markets.

If these individuals were covered, their out-of-pocket costs would skyrocket drastically. Average spending would triple for people with cancer, diabetes, arthritis, high blood pressure or other serious medical conditions such as heart disease and stroke; and additional increases might result from their care being excluded since spending on non-excluded conditions would not count towards meeting deductibles and out-of-pocket maximums of their policy.

Underwriting Rate Increases

Prior to the Affordable Care Act (ACA), individual-market insurers frequently denied coverage to those with preexisting health conditions or charged them much higher premiums – known as rate-up. For instance, Lori could be turned down from coverage by an insurer due to her hypertension, or they might require her to pay substantially higher premiums; moreover, many policies lacked key benefits that were important for people living with health conditions known as carve-outs.

Small group plans typically do not engage in rate-up or carve-out practices and generally provide comprehensive coverage for people with preexisting conditions, though even in these plans one person with preexisting conditions could drive up costs for everyone else in their group due to adverse selection; an insurer who finds itself enrolling more sick individuals than anticipated may need to raise rates to offset part of its underwriting losses and bring profits back into its pockets.

Experience Rating is a strategy used by insurers to avoid adverse selection by using past claims information to estimate current and anticipated medical costs for a policy type and set future premiums accordingly. Experience rating can give an accurate picture of medical costs that pertain to specific policies; however, employers may use experience rating to discriminate against workers likely to incur costly medical bills.

People are increasingly turning to short-term insurance and other non-ACA compliant plans that don’t cover preexisting conditions for coverage, including health care sharing ministry plans, fixed indemnity plans and travel medical coverage. These policies tend to be much cheaper than their ACA-compliant counterparts while still covering preexisting conditions.

TWIA Actuarial & Underwriting Committee met on July 11, and approved a motion that recommends its Board of Directors approve an increase of 5% for 2024 residential policies and 8% for commercial policies at their meeting on August 8. This recommendation is based on TWIA’s annual 2023 Rate Adequacy Analysis prepared by its actuarial staff.

Out-of-Pocket Maximums

The out-of-pocket maximum is a limit on how much of your medical costs you must cover before health insurance starts covering them fully. This figure doesn’t take into account premium payments or your deductible amount, and stands alone as an annual cost cap.

At least until you reach your out-of-pocket maximum, most medical services must be paid for out of pocket; exceptions include preventive services covered without deductible by your health plan. Your out-of-pocket maximum may include your deductible, copayments and/or coinsurance costs; in some plans there may also be a prescription deductible which must first be met before prescription drug costs count toward reaching this maximum amount.

Out-of-Pocket Maximums are part of the Affordable Care Act (ACA), and apply to non-grandfathered individual, family and employer health plans. Their limits are determined annually by the Centers for Medicare and Medicaid Services Office of the Actuary; each limit is calculated based on data regarding individual market health plan premiums as well as overall economy averages; recent years have seen health insurance premiums increasing faster than medical services costs making future out-of-Pocket maximum limits difficult to predict accurately.

The Health Care Reform Law mandates a new cost-sharing arrangement known as cost-sharing reduction or CSR. This type of cost sharing allows your health plan to provide coverage only after reaching a predetermined level of out-of-pocket spending each policy year; typically this amount equals or falls below your deductible threshold.

Once your policy year begins, the out-of-pocket maximum becomes more relevant as time progresses. Once reached, this limit allows your health plan to cover 100% of all services for any individual or family until its conclusion at year’s end.

Maintaining awareness of your out-of-pocket maximums throughout the year and being aware of when they may be reached is important. Your health insurance company should send an annual statement outlining these amounts; using this data you can budget medical expenses effectively while making sure not spending beyond what your maximum allows.

{kind=link}